![]()

Social Security Optimization

Claiming Social Security benefits early comes at a cost.

A University of Michigan report has quantified this to be equivalent to $111,000 per household that is lost due to benefits being taken before full retirement age (FRA). As a whole, retirees are losing $3.4 trillion in Social Security benefits because they chose to “cash in” at the wrong time.

Unfortunately, the Social Security Administration is no help for your client when they file for their benefits. Employees of the Social Security Administration cannot give investment or financial advice. They are only allowed to give straightforward facts revolving around how much you can get when you file at a specific age.

While the “first” retirement goal for many is to maximize Social Security benefits, there are many more factors that play into retirement – like risk, taxes, decumulation, and of course, runway.

What can your clients do to maximize their retirement income?

Why Analyzing Social Security Benefit Scenarios is Important

Every person’s relationship with Social Security is different, which produces different scenarios for retirement. FRA plays a very important part in what happens when a client is planning retirement, enough so that using a technological tool to look at each scenario may be necessary to maximize their benefits.

FRA is dependent upon when your client was born. In most circumstances, the age range falls between 65 and 67. The full range of when a client can file, regardless of FRA, is 62 to 70. The amount of a client’s Primary Insurance Amount (PIA) is their full benefit, calculated by the Social Security Administration (SSA). The SSA comes up with the amount based on the Average Indexed Monthly Earnings (AIME) for the 35 years of highest earnings.

Claiming Social Security Benefits Early

Those clients who choose to claim benefits early and don’t wait are penalized with a reduction of 20% to 30% based on their FRA. The benefit reduction is calculated at 5/9 a percent per month for the first 36 months. After that, it is 5/12 of a percent for each additional month.

| Reduced PIA by Age | 65 FRA | 66 FRA | 67 FRA |

|---|---|---|---|

| 62 | 80% | 75% | 70% |

| 63 | 86.7% | 80% | 75% |

| 64 | 93.3% | 86.7% | 80% |

| 65 | 100% | 93.3% | 86.7% |

| 66 | N/A | 100% | 93.3% |

| 67 | N/A | N/A | 100% |

The chart shows the percentage of benefits for clients who decide to take their Social Security benefits before the FRA. For clients who might be considering filing for Social Security benefits early, seeing what it does for their retirement income may change how they approach the situation.

Delaying Social Security Benefits

On the flip side, those clients who want to delay taking their Social Security benefits look to receive an incentive, “delayed retirement credits” (DRCs), for doing so. The DRC adds approximately 2/3 a percent per month to your client’s benefit – ultimately based on their birth date.

Effect if Delayed Retirement Credits on PIA

| Year of birth | % of PIA at age 70 |

|---|---|

| 1941 | 132.5% |

| 1942 | 131.3% |

| 1943 – 1954 | 132% |

| 1955 | 130.7% |

| 1956 | 129.3% |

| 1957 | 128% |

| 1958 | 126.7% |

| 1959 | 125.3% |

| 1960 | 124% |

Strategies to Help Clients Collect Maximum Benefits

By optimizing Social Security filing, you help your client collect the maximum amount they are entitled to while also considering the overall retirement income they will need for the future. Social Security income is a factor to consider in the overall unified managed household, especially when considering future retirement income. Seeing different scenarios can help your firm advise clients correctly on a plan of action – with Social Security as a piece – to live comfortably during retirement.

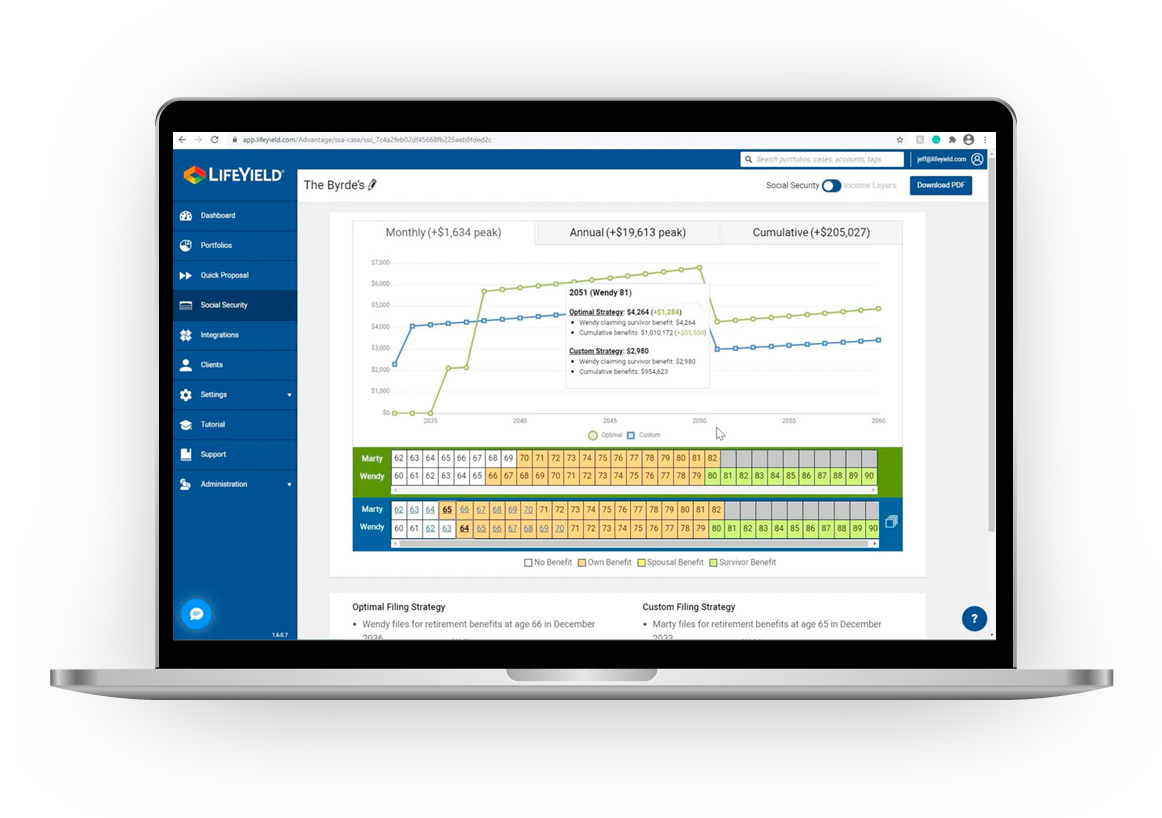

Going Beyond Social Security with SEI LifeYield Social Security+

The core component of SEI LifeYield Social Security+ allows for firms and advisors to compare multiple filing strategies for clients. What would retirement income look like if your client retired early? What if they wait until age 70? At what age can I comfortably start claiming Social Security benefits when all factors are taken into account?

SEI LifeYield can answer those questions. But when it comes to Social Security, many investors think it will be a more substantial piece of the retirement income pie than it really is.

Social Security should be considered part of the plan. Not the whole plan.

With SEI LifeYield, all of the different Social Security scenarios can be visualized. And you can flip on the Income Layers add-on to visually pair the client’s optimal filing strategy with the rest of your client’s retirement income streams.

How SEI LifeYield’s Social Security+ Works: A Case Study

Meet Sally, a 60-year old accountant from Kansas. She has never been married, has no children, and has always been extremely career-focused. Thanks to Sally’s knowledge of investing, she has created quite a retirement portfolio of her own – but she doesn’t know a lot about Social Security.

Since Sally has spent all her time in Kansas, she wants to spend a good portion of her retirement traveling the world, seeing all the sights she missed out on during her working years. She comes to your firm for help.

With SEI LifeYield Social Security+, you can help Sally peer into her financial future by walking her through the benefits and drawbacks of taking her Social Security benefits early.

Based on Sally’s estimation, she needs to collect at least $80,000 a year (after initial travel investments) to live comfortably. With that said, you begin running the calculations to see when the best time is for Sally to collect Social Security to meet her retirement needs.

Using SEI LifeYield to Optimize the Overall Filing Process

Not everyone’s situation will be like Sally’s. Not everyone thinks to plan for their future. If you delay taking benefits, can you still retire? How will you fund the years you’ll spend without a paycheck? Using SEI LifeYield, your firm can look across all client accounts and show clients when (and how much they need) to fill income gaps in retirement. This presents an opportunity to position other retirement income products like life insurance and annuities.

SEI LifeYield was created to enable the unified managed household by increasing overall tax efficiency and maximizing Social Security. Social Security is a key piece of retirement for many Americans. But it needs to be coordinated with all other streams of retirement income to achieve the best possible results for the client.

Technology creates client trust. And that trust is important to building sticky relationships that last a lifetime.

For educational purposes only. This information should not be considered investment advice.